|

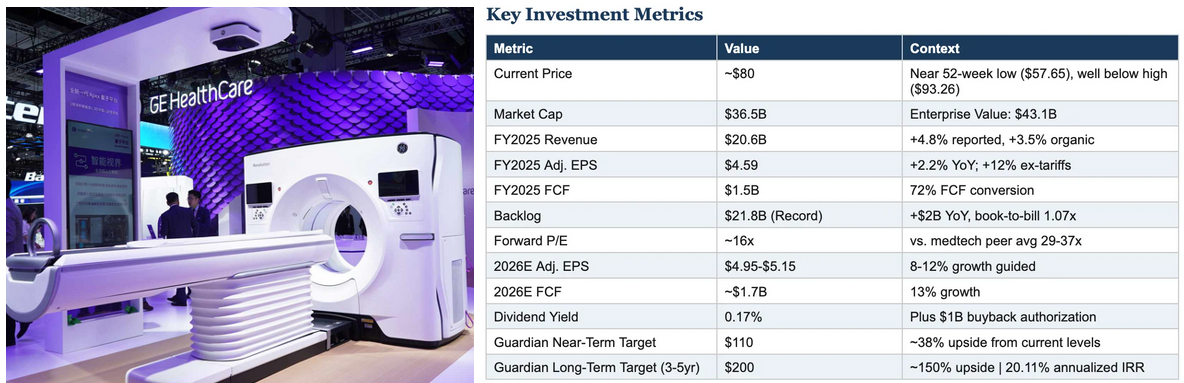

Guardian Research has published a very comprehensive report on GE Healthcare (click). The "dismantling of GE" is major success story: GE Aerospace has doubled, GE Vernova is 4x. The Healthcare segement is up 40% since spin-off. As the "GE-stigma" is fading slowly, the benefits of being independent start to materialze. China and tariff risk have held back the development temporarily. But vitality rate (55% of products are younger than 3 years) and the opportunities of AI-enabled healthcare (huge data moats) are about to unfold. Guardian Research sees 12-18% EPS CAGR (vs street 8-10%) and long-term upside of 150%. If correct, can Siemens Healthineers (trading at 5-year-low) follow the trajectory? Like Siemens Energy followed GE Vernova´s rally since spin?

Constellation Software stock has halved within 8 months on "AI disruption risk" for vertical software. Tidefall Capital is looking at RBCs defense of CSU. Key argument is that even is AI is fully disruptive of the CSU model (which is far from a sure thing), this is now embedded in current price. As the model does not depend on terminal value, harvesting near-term cash flows is enough to justify current price. If the model is not obsolete, depressed vertical software prices make cheap acquisitions and future value generation possible (click)

Hated Moats thinks that the ~70% sell-off over 1 year in WIX.com is overdone (click). The shares are now trading 25% below his bear-case scenario. The company is buying back 40% of the market cap. The bet is that SME client relationships are sticker, hence ample FCF streams more durable, than (potential) full AI-disruption scenarios imply. German peer Ionos is also down 45% from recent highs

Iggy pitches Global Dominion, a Spanish engineering firm in transformation (click). They are selling their asset-heavy renewables business and become an asset-light, highly free-cash-flowing business with multiple expansion potential (vs peers like Bilfinger, SPIE). The current EV of EUR 500mio under-represents the EUR 100mio FCF potential post-transformation. There´s 12% insider share-holding, among them Basque business titan Antón Pradera Jáuregui (sold INSSEC to Tecnicas Reunidas).

Under-Followed-Stocks profiles Circle SpA, an Italian Micro Cap, operating the digital infrastructure behind ports and intermodal transport. It´s an owner-operator company in a niche that is too small for big software / tech companies, and too complex and regulatory demanding for the proprietary solutions currently used by local authorities. Reminds me of Frequentis (click)

|