|

|

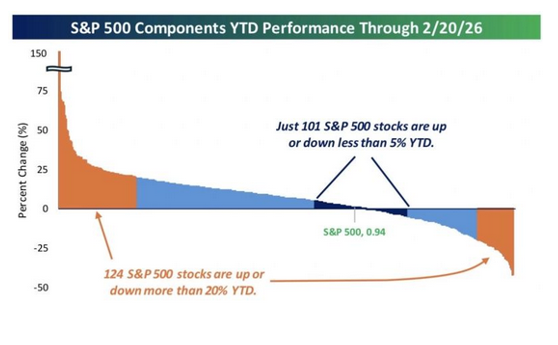

Big things happen under the hood: Some 124 SPX stocks are either up or down 20% ytd

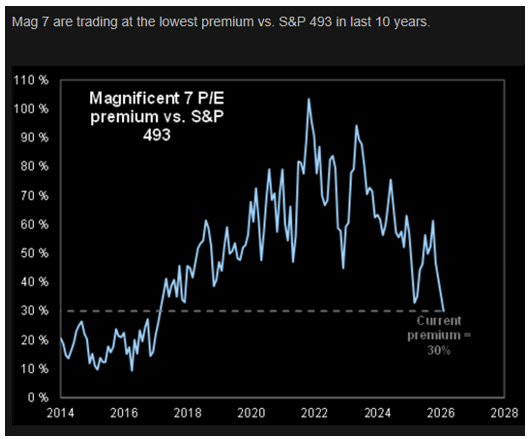

Mag7 PE-premium vs the "Rest of the market" is at a 10 year low. Market falls slightly, index concentration eases..

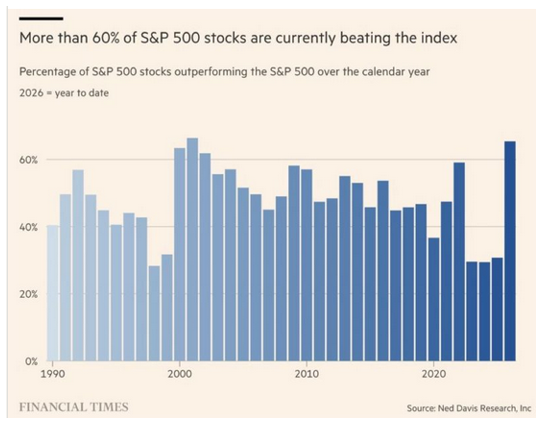

...more stocks outperform....

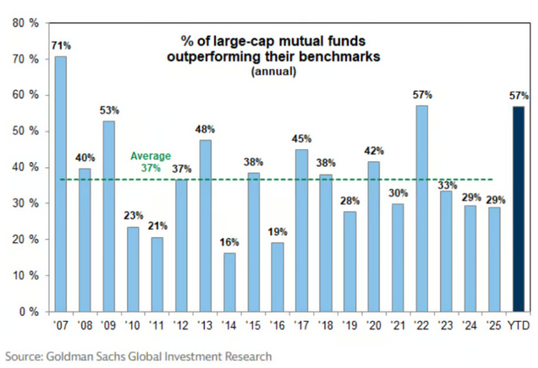

...more active managers outperform. To me the big question is: what happens to the overall market when a) Mag7 and Tech keep sliding and b) the rest of the market also gets expensive (driven up quickly by Mag7 / Tech outflows)? The new darlings are called "HALO" (“heavy assets, low obsolescence”) businesses—aka companies that seem relatively immune to automation, like McDonald’s or John Deere—are the new safety stocks. But: Consumer Staples are now trading at a higher PE multiple than the Tech Sector....

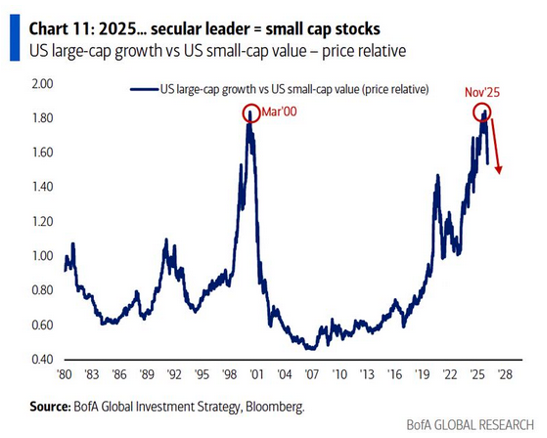

As this is primarily a US Large Cap (one might also say ETF) situation, Small vs Large is turning...

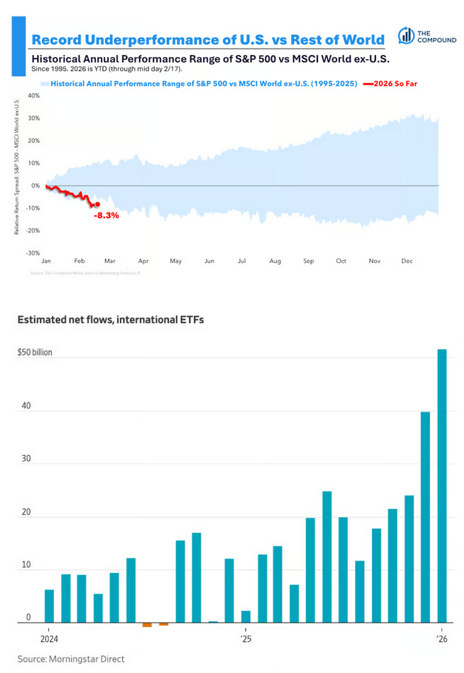

...and RoW vs US is turning. In this context, please also watch Miller Value presentation in the video section

|

|

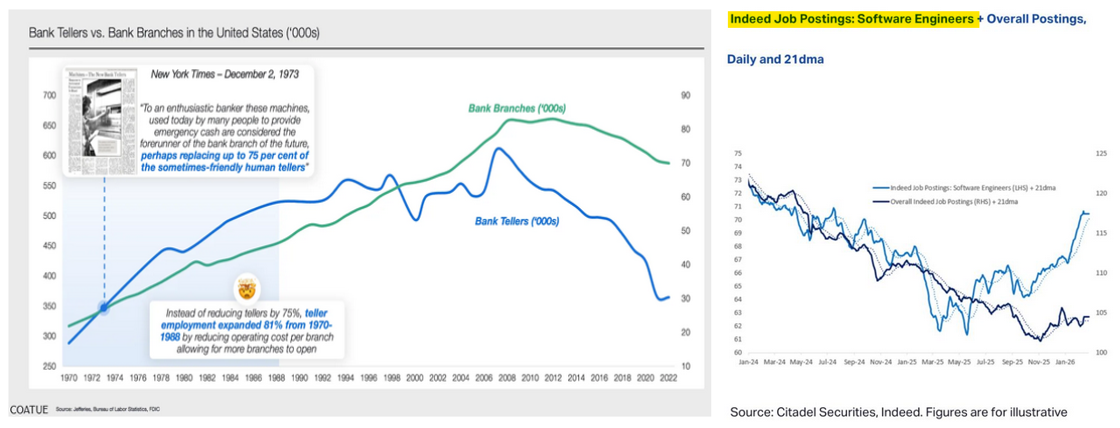

AI fear is everywhere. See Citrini report earlier this week (click). "We´re all going to be replaced by AI and robots". Yet historically, more efficiency has initially led to massive job growth (see "bank teller paradox" below; source: Coatue). More generally, economist speak of Jevon´s paradox (more efficiency leads to exponentially higher deployment, more use cases, etc; illustrative: number of software engineer jobs sharply up since July25). Now: from an investing perspective things are even more complicated. Heavy Moat Investing looks at the risks of being contrarian in light of AI (see article above).

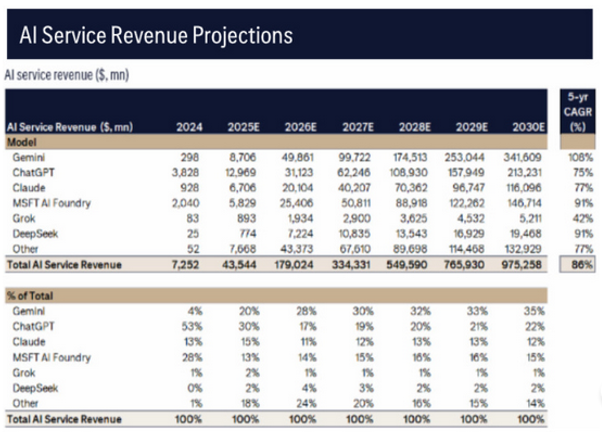

The estimated AI service revenue hockey stick (source Citi). One point I haven´t heard yet in the discussion: If the LLM providers know that compute will be commoditized, they also know they need to go into software, beyond just offering APIs, in order to achieve approriate returns on their investments. And if they really build their own verticals and try to replace the software incumbents, what about antitrust regulation? Why should regulators allow them to own the rails and the trains, for quasi-monopolistic profits? Note that the key players (GOOG, MSFT/OpenAI, AMZN/Anthropic, Meta) are already under anti-trust scrutiny in other aspects of their business. One might argue, they can only fund these investments because of their (over-) dominant market positions in other businesses. Why is nobody discussing this aspect?

Meanwhile, talking about hockey sticks (click)

Cassie Kazyrkov at Decision Intelligence thinks the the promise of AI is also its peril: "you can get results without putting in as much thought and effort along the way. AI will amplify our mistakes and our poor judgment if we’re not careful". This seems especially relevant for investing: you cannot borrow conviction from AI. Good judgement gets exponentially more valuable.

5 Investment Write-ups worth your time

|

|

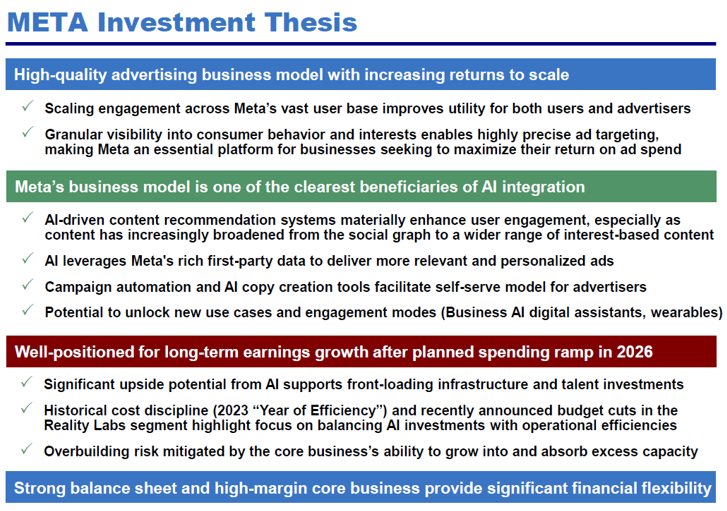

Bill Ackman´s / Pershing Square´s annual presentation contains his new Meta thesis (also: Uber, UMG, Brookfield, GOOG, Hilton, Hertz). They put 10% of their fund or USD 2bn into Meta, calling it "deeply discounted" with underappreciated AI upside

Jeremy Stern has written a brilliant portrait of Palantir COO Shyam Sankar. Don´t get me wrong: I have real political and moral concerns regarding this company and its leaders. But this portrait reads like a very, very good book. The personal side is breath-taking. The insight into what Palantir actually does and how Sankar literally willed it into operating existence (as its first "forward deployed engineer") are very insightful. You got to know the enemy... Jeremy Stern has written a brilliant portrait of Palantir COO Shyam Sankar. Don´t get me wrong: I have real political and moral concerns regarding this company and its leaders. But this portrait reads like a very, very good book. The personal side is breath-taking. The insight into what Palantir actually does and how Sankar literally willed it into operating existence (as its first "forward deployed engineer") are very insightful. You got to know the enemy... Kevin Koharki shows how big Tech Firms like Meta actually spend more than double of what they disclose on SBC. A gravy-train of wealth redistribution from shareholders to employees / management. Non of the disclosure is illegal or falty, it´s all within the rules. Yet, the resulting display of FCF (and the multiples attached to it) lead to these gigantic valuations. Taken private, these companies would be worth much less, assuming they had to pay cash to their employees. See podcast below Kevin Koharki shows how big Tech Firms like Meta actually spend more than double of what they disclose on SBC. A gravy-train of wealth redistribution from shareholders to employees / management. Non of the disclosure is illegal or falty, it´s all within the rules. Yet, the resulting display of FCF (and the multiples attached to it) lead to these gigantic valuations. Taken private, these companies would be worth much less, assuming they had to pay cash to their employees. See podcast below

|

|

Ray Dalio has a Substack now

JPM has a pub in its HQ. Meanwhile, real pubs are dying left, right and center. 14k in the UK alone. Data Geek Lauren Leek is looking at the reasons and explains why this is a real loss for society (click). As my late grandad always said: Put down the phone, go down the pub, speak to real people. Lots of problems would not exist if people would talk more in real life. Go down the pub this weekend ! What a legend What a legend Enjoy the Weekend! Enjoy the Weekend!

|

|

This message is confidential and intended for the recipient and for the exchange of information only. Legally binding declarations are not accepted by this means of communication. If you are not the intended recipient, please contact the sender and delete the message and any attachment from your system. In this case you must not copy this message or attachment or disclose the message to any other person. The company cannot accept any liability for the accuracy or completeness of this message. This is not investment advice. Do your own research !

|

|

|

|

|